The escalation of the Middle East conflict has triggered diverse and sharp drops in travel security perception across Gulf destinations, prompting early signs of demand diversion among European and US travellers towards closer-to-home and long-haul alternatives, according to latest analysis of Mabrian (part of Almawave – Almaviva Group). US travellers are particularly sensitive to security concerns, while neighbouring destinations such as Egypt, Türkiye, and Jordan are feeling spillover effects on traveller confidence.

Mabrian’s latest travel intelligence comparative analysis of security perception across key Middle East destinations and outbound demand trends reveals that the escalation of the Middle East conflict is prompting early signs of demand diversion in key European and American source markets, against a backdrop of sharply deteriorating security perception across Arab Gulf and neighbouring destinations.

For this analysis, Mabrian by Data Appeal is examining traveller behaviour and sentiment, and three-month trends from the United Kingdom, Germany, France, Italy, and the United States—five key non-regional outbound markets for GCC destinations—as well as for major destinations within the conflict’s sphere of influence, including Egypt, Jordan, and Türkiye.

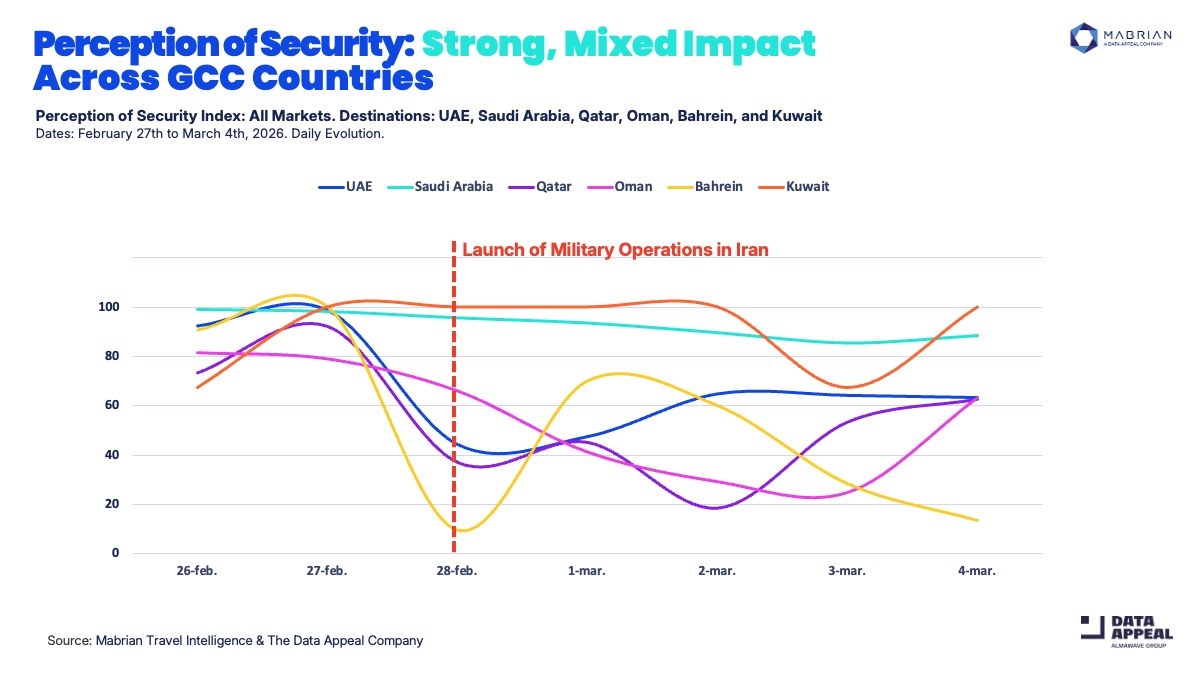

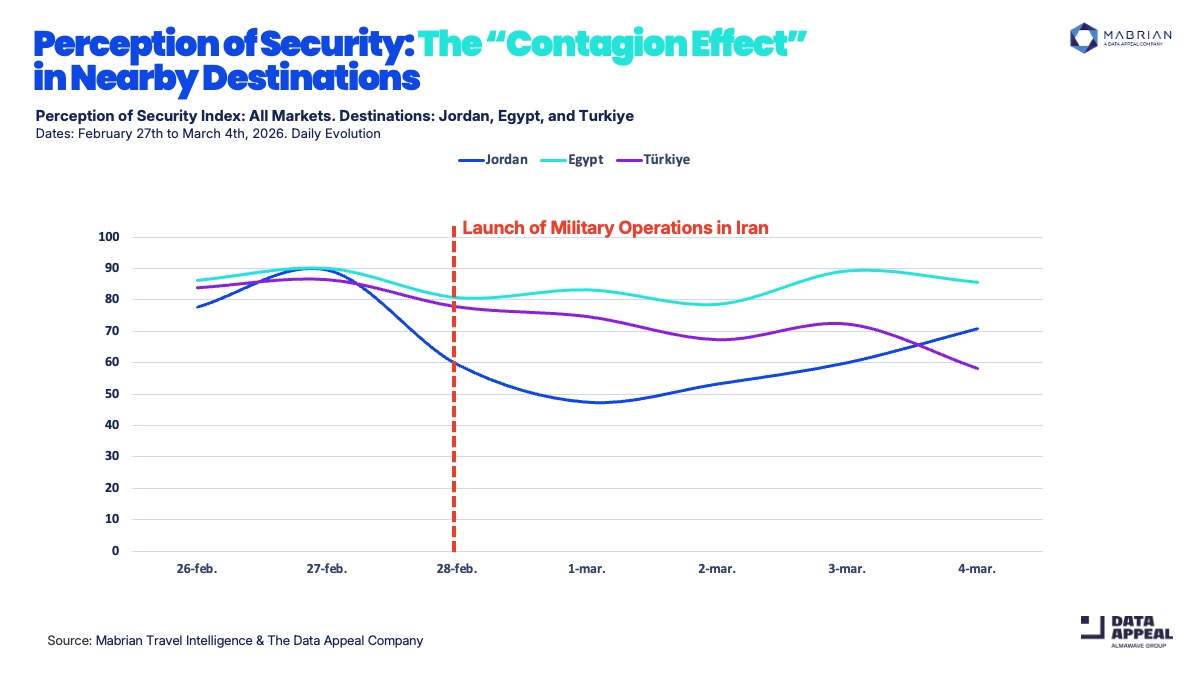

The latest evolution of Mabrian’s Perception of Security Index (PSI) over the past month, up to 4 March, indicates a pronounced deterioration in travellers’ safety sentiment across GCC destinations, with varying intensity by country. Egypt, Jordan, and Türkiye are also impacted, albeit to a lesser extent. These markets—particularly the Arab Gulf states—have invested considerable effort over the past decade in consolidating security as a core reputational pillar, achieving consistently high and, in some cases, exceptionally resilient scores.

Overall, the findings highlight the vulnerability of security perception as a strategic reputational asset, given its high sensitivity to geopolitical tensions. These are the key trends data unveil:

- Acute Yet Divergent Impact on GCC Destinations: Following the commencement of military operations in Iran on 28 February, PSI scores across GCC markets—particularly those geographically proximate to the conflict and reportedly targeted—registered the steepest declines. Starting from robust benchmarks one month prior, Bahrain experienced a contraction of -81 points (out of 100), falling to a low of 9.6. Oman recorded a similar downturn, shedding -56.7 points to reach 24.8/100 at its lowest level. Qatar declined by -54.9 points, bottoming at 18.4/100. Among these, Bahrain and Oman are encountering greater difficulty in regaining lost ground, whereas Qatar—alongside the UAE and Saudi Arabia—has begun to partially absorb and stabilise the shock. The United Arab Emirates and Saudi Arabia, although adversely affected, have demonstrated comparatively stronger resilience. The UAE registered a -48.3-point reduction, reaching a low of 51.9/100, while Saudi Arabia declined by 13.6 points, bottoming at 85.3/100. Despite these decreases, both destinations avoided the sharper contractions observed elsewhere in the region, underscoring comparatively higher robustness in perceived stability.

- Contagion Effect in Neighbouring Destinations: Egypt, Jordan and Türkiye—while not directly involved—are experiencing a spillover or “contagion effect” attributable to their geographical proximity and perceived exposure to the conflict’s sphere of influence. Jordan, which stood at 77.6/100 a month ago, lost -30.3 points at its lowest reading, although it is now exhibiting gradual signs of recovery. By contrast, Türkiye’s PSI declined by a comparatively moderate -25.8 points (from a peak of 83.8/100), yet the trajectory does not currently indicate a rebound. Egypt remains the least impacted among the three, with a contraction of 7.6 points, still showing no stable recovery signs.

- Heightened Sensitivity Among US Travellers: A common denominator across all analysed destinations is the pronounced reaction among US travellers, whose safety perception has proven more sensitive than that of other key long-haul source markets. The PSI among American travellers recorded substantial contractions: Kuwait dropped by -87.3 points, the UAE by -79.2 points, and Saudi Arabia by -17.8 points. Current trend lines suggest limited prospects for short-term recovery in these segments. Egypt’s trend is similar, as this destination also registered stress within the US market, with a -32.6-point decline at its lowest level and an unsteady recovery trajectory.

As Carlos Cendra, Director of Marketing and Communications at Mabrian, observes: “These destinations have worked meticulously to position themselves as stable and secure environments. In fact, our forecast for early 2026 showed that Western Asia was gaining market share in international travel demand, with three GCC cities ranking among the world’s top 10 destinations for growth in travel intent during the first half of the year. This sudden trend shift highlights how crucial it is for destinations to closely monitor travellers’ perceptions — particularly safety sentiment — an extremely strategic, yet inherently fragile and volatile asset.”

“From a long-term destination management perspective, restoring confidence will become an immediate strategic priority once the conflict subsides, especially as international travel demand is already showing early signs of diversion,” says Mabrian’s spokesperson.

Middle East Conflict Triggers Early Diversion of International Travel Demand

Mabrian data intelligence shows that, amid the Middle East conflict and worsening security perception, three potential travel demand diversion scenarios are emerging across key outbound markets — the UK, Germany, France, Italy, and the US.

The first points to a growing inclination to remain closer to home. This tendency is particularly evident among German travellers—who are prioritising destinations such as Morocco and Greece—alongside Italians, whose interest is shifting towards Croatia, the Czech Republic, Norway and Spain. British travellers are showing a similar pattern, with Malta, Morocco, and Montenegro gaining prominence as alternative options.

A second scenario highlights the continued strength of demand for Asia, supported largely by direct air connectivity. Interest remains particularly robust for destinations such as Japan, Thailand, Vietnam, Cambodia and the Philippines. The materialisation of this demand, however, will largely depend on the extent to which airfares on these direct routes remain competitively priced and attractive.

Finally, several long-haul destinations are emerging as potential substitutes. Among British travellers, South Africa and the Maldives are gaining traction, while Latin American destinations are attracting attention from French, Italian, German and US travellers. In particular, Peru and Brazil are appearing as aspirational, “bucket-list” alternatives.

Another notable trend is also emerging within European demand: Egypt continues to maintain its appeal among German, Italian and French travellers; however, this demand remains highly exposed to developments in the Middle East conflict. As explained by Cendra: “Travel advisories, restrictions affecting connectivity, or limitations on access to key tourism areas could rapidly influence travellers’ perceptions and, consequently, their willingness to select Egypt as a destination.”

As Mabrian expert highlights: “In times of global uncertainty, relying on data intelligence is essential. Monitoring travel and tourism dynamics — from evolving air connectivity to traveller perceptions and other key indicators — provides destinations with the insight needed to navigate any crisis, guide recovery efforts, make informed decisions, and respond strategically to shifting demand patterns.”